Miller Robinson usually shops at Publix, but a trip to Winn-Dixie in 2010 to purchase a pint of ice cream led to something more than a sweet treat — a $15,195 reward.

Robinson noticed the store clerk did not charge him sales tax on the pint. He was familiar with Florida’s sales tax law, and knew that while most groceries are exempt from sales tax, ice cream, frozen yogurt and similar frozen dairy or nondairy products in cones, small cups or pints, are not.

After reporting the violation to the Florida Department of Revenue in hopes of receiving an reward, Robinson received a generic letter telling him he did not qualify.

Sales tax is one of 18 types of Florida taxes and fees that consumers who spot a violation can report to the state in hopes of being paid a reward. The compensation is paid from back taxes the Department of Revenue collects in each case, and can be anywhere from 5 percent to 10 percent.

“I knew that was wrong. The reward can vary and can be up to 10 percent of what they collect in back sales tax,” Robinson said. “I called the man in charge of the rewards program. He was very nice and helpful, and said, ‘Miller, I will get to the bottom of this.’ He read those people the riot act.”

Eventually Robinson received the reward money for reporting the Winn-Dixie violation.

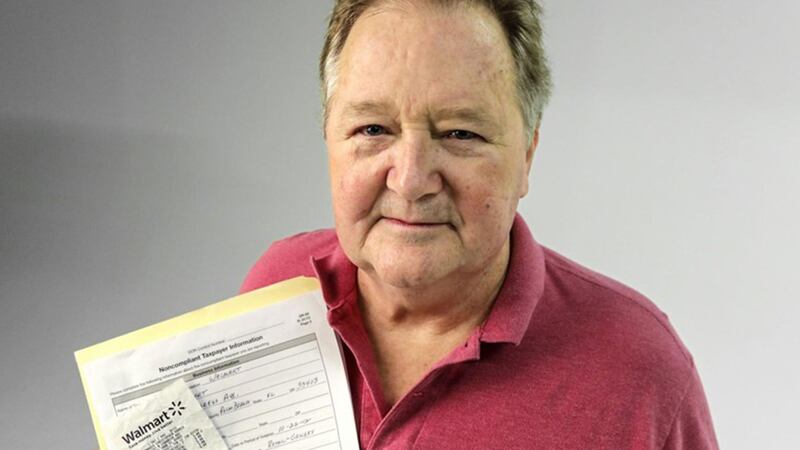

But Robinson’s attempt to collect a reward for the same issue with a 2012 purchase at Walmart was not successful. He purchased a pint of ice cream at Walmart, and he said he was not charged the sales tax required by law.

He filed a complaint with the Department of Revenue, but according to a Nov. 19, 2014, letter he received from the rewards program, the information he provided did not result in the collection of any money so he would receive nothing. The case was closed, and state officials made that clear in a number of letters to Robinson.

The 2014 letter states that while the DOR cannot provide specific information, there are a number of reasons why a reward isn’t issued. For example, the tax owed could have been paid before the reward claim was filed.

But Robinson isn’t convinced. During a two-year period Robinson was told an audit was under review.

“They let the big fish off the hook,” Robinson said.

Walmart officials did not respond to a request for information about the receipt.

Department of Revenue spokeswoman Valerie Wickboldt said this month that under Florida law taxpayer information received by the department in returns, reports and accounts is confidential.

“An informant would be prohibited from receiving confidential information or updates on the actions taken by the Department in regard to a taxpayer, other than the amount that may have been collected as the result of the information that the informant provided, and the amount that the informant will receive,” Wickboldt said.

Taxes on ice cream pints are among the many little-known quirks in Florida’s sales tax law.

“It’s hell for retailers,” said James Sutton, an attorney with Moffa, Sutton & Donnini with offices in Fort Lauderdale, Tampa and Tallahassee. The law firm represents retailers in sales tax cases.

The Department of Revenue collects more than $200 million a year in back sales taxes from businesses, Sutton said.

There are also 17 other types of taxes and fees, from communications services to the new tire fee, in the Department of Revenue’s rewards program. Anyone who provides information leading to the registration of a non-compliant taxpayer and/or the collection of taxes, penalties and interest can receive compensation.

“Publix is smart enough about this that it will take in its register every six months and get the Department of Revenue to bless how they are doing it,” Sutton said.

“If you go to Dunkin’ Donuts, there will be a sales tax on one doughnut but if you buy three, there is not,” Sutton said. “The line in the sand says if you buy one, you are eating it on the premises,” Sutton said.

The premise is that eating the doughnut at the bakery is a restaurant meal, not a grocery item.

The law exempts food and beverages that will be taken home to be consumed, but not those expected to be consumed on the premises.

The states’s sales tax policy provides that bakery products sold by bakeries that do not have eating facilities are exempt.

“There are six different ways to tax or not tax popcorn kernels. If you buy unopened kernels in a can, you will not be eating on the premises,” Sutton said. “If you buy it popped and hot in the grocery store, you will be taxed.”

With the sales tax, the intent is to not tax Florida residents on necessities, Sutton said.

“The laws are designed to exempt residents and tax tourists,” Sutton said.

That is the thinking behind why food purchased at restaurants is subject to sales tax, but most food purchased in stores is exempt.

“If you visit Florida on vacation, you will pay sales tax on rent. If you rent for six months and a day, you have become a legal resident, and you don’t have sales tax on it,” he added.

The exemptions and rules extend far beyond groceries, and the burden of proof is on the retailer.

Take furniture sales. Sales tax does not have to charged on furniture shipped out of state. But the retailers must keep receipts to prove where the shipment went.

“If you don’t keep shipping records, you owe the taxes,” Sutton said.

Office supplies are subject to sales tax. If a business is audited, it has to prove it paid the taxes.

Sutton said sales tax is a “very strange” area of law.

In the past, if retailers were in doubt, they would charge the sales tax. Then, if customers could prove they should not have been taxed, they would get a refund.

Now, with class-action lawsuits over sales taxes on such items as pizza delivery fees and discount coupons, the retailers have that worry also.

“If I charge too little tax, the state will come after me. If I charge too much tax, the class-action lawyers will come after me. I have to spend a lot of money to make sure I am doing it right, and that all the employees are trained,” Sutton said.

Florida’s sale tax quirks

Here’s a few of them for items sold in grocery stores:

Tax exempt Subject to taxes

Drinking water Water with carbonation or flavoring added, bagged ice

Orange Orangeade

Marshmallows Candy

Tea bags Tea sold in liquid form

Sandwich prepared Sandwich prepared in the store

off the store’s premises

Quart of ice cream Pint of ice cream

Vegetable salad, fresh Vegetable salad, cooked, with utensil

Source: Florida Department of Revenue

Section 213.30, Florida Statutes, authorizes compensation to someone who provides information leading to the registration of a non-compliant taxpayer and/or the collection of taxes, penalties, and interest with respect to the following taxes and fees:

Communications Services

Corporate Income

Estate

Documentary Stamp

Fuel Taxes on motor, diesel, aviation, and alternative fuels, including local option taxes

Government Leasehold Intangible Personal Property

Gross Receipts Tax on dry-cleaning services

Gross Receipts Tax on natural or manufactured gases or electricity

Insurance Premium Taxes, fees, regulatory assessments, excise taxes, and surcharges required to be remitted to the Department

Intangible Personal Property Tax

Local Option Convention Development Tax, Tourist Development Tax and Tourist Impact Tax when the imposing local government has not elected to self-administer the tax

Miami-Dade County Lake Belt mitigation and water treatment plant upgrade fees

Motor Vehicle Warranty Fees

Pollutants

Rental Car Surcharge

Sales and Use Tax and Local Option Discretionary Sales Surtaxes

Severance Taxes, Fees, and Surcharges on gas and sulfur production, oil production, solid mineral severance

Solid Waste Fees, including the New Tire Fee, and the New or Remanufactured Lead-Acid Battery Fee

Examples of taxes that are not included in the program (not an all-inclusive list):

Local Option Convention Development, Tourist Development, and Tourist Impact when the imposing local government has elected to self-administer the tax

Property

Reemployment (Unemployment)

For more information contact the tax violations unit at TaxViolations@floridarevenue.com or call

Within Florida: 800-352-9273

Outside Florida: 850-717-6994

Cox Media Group